What Is The Base Rate (BR) And Base Lending Rate (BLR) All About?

The Base Rate (BR) is an interest rate that the bank refers to, before it decides on the interest rate to apply to your home loan. Prior to 2015, that interest rate was referred to as the Base Lending Rate (BLR). Here’s all you need to know about it!

For example, you may be wondering what the terms ‘BR’ and ‘BLR’ actually mean. Well, wonder no more as we dive into these two important terms!

Base Rates and BLR in Malaysia

The Base Rate (BR) is basically an interest rate that the bank refers to before it decides on the interest rate to apply to your home loan.

The rate is derived internally within the bank based on how much it will cost the bank to lend you the money, and takes into account a minimum interest rate set by Bank Negara Malaysia (BNM).

Before 2015: Base Lending Rates (BLR)

Prior to 2015, the interest rate was referred to as the Base Lending Rate (BLR). This BNM rate is based on the overall financial health of all financial institutions in Malaysia.

BNM also used the Overnight Policy Rate (OPR) as a benchmark to determine the cost of lending money.

Derived through a blanket formula that applies across the board, the BLR was determined after reviewing the Statutory Reserve Requirement (SRR).

The purpose of implementing the BLR system by BNM was to ensure a fixed and somewhat predictable interest rate across all banks in Malaysia.

If you buy a property using Islamic loans, your BLR is referred to as the Base Financing Rate (BFR).

The process is pretty transparent and you can find the latest rates online. Packages across the different banks are usually rather similar.

2015 onwards: Base Rates (BR)

The new Base Rate system, which came into effect in January 2015, made things more competitive for financial institutions.

The Base Rate is calculated against each bank’s cost of funds and Statutory Reserve Requirement (SRR), along with the borrower’s credit risk, liquidity premium, operating cost, and profit margin.

In short, banks in Malaysia can now determine their own interest rate based on a formula set by the central bank and using the BNM rate as a benchmark.

Although the formula is set by Malaysia’s central bank, each bank is able to package better deals for its customers without intervention from BNM, depending on business vitality and type.

For example, if the bank is performing well in the consumer banking sector, they would be able to offer more attractive home loan packages.

Why do Base Rates change, and how does that affect me?

As mentioned above, many factors impact how banks decide their Base Rates. Most importantly, you need to know that Base Rates are pegged to Bank Negara’s Overnight Policy Rate (OPR).

Despite that, do know that unlike the previous BLR, banks can adjust their respective Base Rates even when there is no change in the OPR.

The Overnight Policy Rate (OPR) is the minimum interest rate at which banks lend money to each other. Hence, when the OPR is cut, banks will lower their Base Rates accordingly. When Base Rates are reduced, so will the cost of borrowing for us consumers.

This means that for average Malaysians like you and me, we get to enjoy lower interest rates on our loans. This would then be the best time to take out a loan or refinance an existing one – whether that be a personal, auto or home loan.

In this regard, fluctuations in Base Rates will affect the property market too. With lower Base Rates, home loans will subsequently be offered with lower interest rates.

Typically, developers will also come up with various promotions and discounts during this time to encourage consumers to buy too.

Homebuyers who have been looking to buy a home should then take advantage of this buyer’s market to nab the property they’ve been eyeing!

The effect of the new Base Rate system on home loans approved before 2015

You may be wondering: How will the new Base Rate system affect you if you’ve been paying your home loan for the past eight years?

Since the loan agreement was signed prior to the new rule, the interest rate for home loans approved prior to 2015 will prevail.

It also depends on the agreement that you signed with the bank. If you’d like to take advantage of more attractive packages offered by the bank or other financial institutions, you’ll need to speak to your banker on refinancing options.

Currently, it’s a requirement for all banks to display both BLR and BR on their websites and bank branches.

How will the Base Rates in Malaysia affect your home loan?

The key reason for this new system implemented by BNM was to offer better transparency.

Heightened transparency would translate to better-informed consumers, thereby benefiting both property owners and consumers in Malaysia.

On 20th March 2020, BNM announced its intent to decrease the SRR from 3.0% to 2.0%, in order to boost the liquidity into the banking system. Although the Base Rate varies from one bank to another, the rate often stays within a loose bracket.

Before the bank decides on the Base Rate it offers, it takes into consideration the cost of funds, which fluctuates across banks, as well as other administrative costs.

The Base Rate also hinges on whether the bank bases the loan agreement on a fixed interest rate or a floating one.

With a fixed interest rate property loan, the Base Rate is predetermined, and the bank has taken on the risk of future fluctuations.

Usually, the banks will charge a premium in place of the risk. So, a floating rate property loan is generally cheaper than a fixed one.

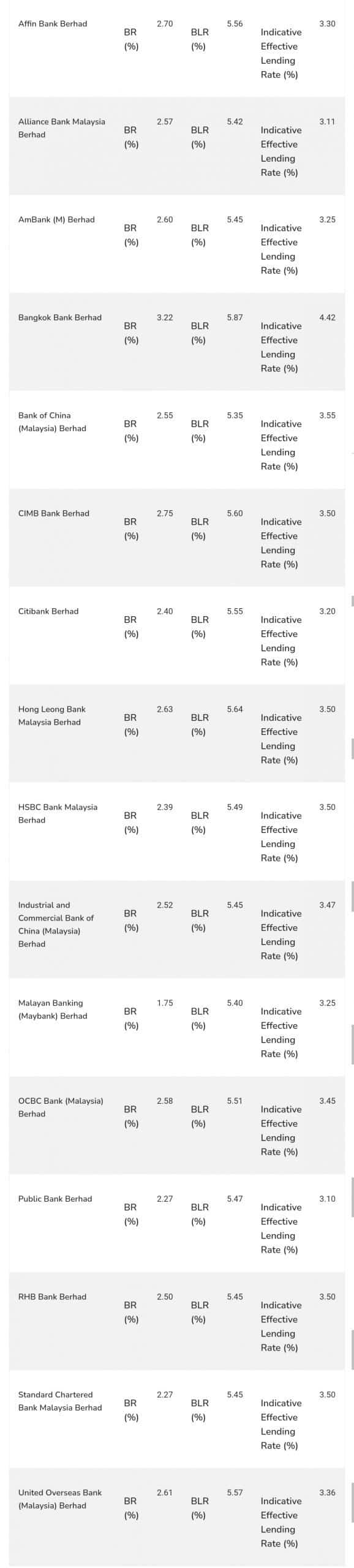

Here’s a table of the latest Base Rates, BLR, and Indicative Effective Lending Rates (taken from BNM), which may come in handy for you:

Latest Base Rates and BLR Updated on 6th August 2020

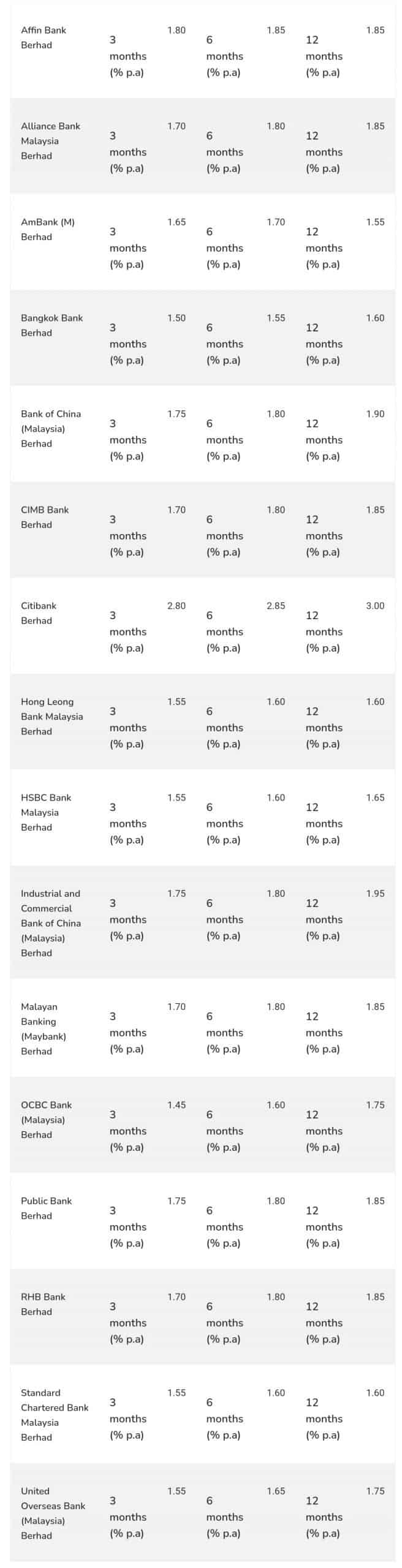

Latest Fixed Deposit Rates Updated on 10th November 2020

OPR cuts will negatively affect Fixed Deposit (FD) Rates. An OPR cut will reduce the FD rates, so one can expect a drop in interest earnings. Keep in mind however, that the final rate is dependent on the individual bank, amount deposited, type of FD and many other factors.

Check out this table below for the latest conventional Fixed Deposit Rates from all banks.

What else should you look out for when buying a property?

Remember that depending on the liquidity and financial records of the bank, the Base Rates can be reviewed at any time, even if there are no changes made to the OPR.

Also, note that the bank has the discrepancy to decide on the amount of interest to apply to a certain group of people, based on their level of credit risk.

If a borrower has a bad credit rating, the bank may or may not impose a higher interest rate.

While the BR is a key area to consider, here’s a list of other important things to note before purchasing your new home:

- Your Debt Service Ratio (DSR): This ratio will determine how much income you can set aside every month to service your loan.

- The reputation, liquidity, and financial stability of the bank:�It’s always prudent to perform research beforehand on the bank you intend to loan from.

- Tenure of the loan and lock-in period: The bank will establish the time period for you to pay off the loan. While this may vary, banks generally set a tenure of 30 years. An Early Termination Penalty is usually imposed for early settlements, including loan refinancing.

- Mortgage Reducing Term Assurance (MRTA): It may be wise to consider getting an MRTA. This is essentially an insurance on your home loan, which helps reduce and pay off the home loan in the event of your injury, disability, or death.

- Maintaining your current BLR in Malaysia: Since most residential property loans signed before 2015 will continue to be referenced by its BLR until the loan matures, write to your bank to request a stay of action.