Standardised Base Rate (SBR): What You Need to Know

Navigating home loans can be tricky, what with complicated jargon and the different types of interest rates to take note of. Add in fluctuating rates and figures, and it can be confusing to calculate the exact cost when you’re planning to buy a home.

Well, those calculations might just be easier moving forward!

Effective 1 August 2022, Bank Negara Malaysia (BNM) announced that the Base Rate (BR) will be replaced by the Standardised Base Rate (SBR), following the revised Reference Rate Framework. Hence, the SBR will now follow the Overnight Policy Rate (OPR) in tandem.

We can see the wheels turning in your head right now. Will the change from BR to SBR affect your loans? What kind of loans are affected by this change? Is SBR the villain or hero of your story?

Worry not because we’ll dive into what SBR is all about and answer your questions.

What Is Standardised Base Rate?

A new introduction to the family, the SBR is a common reference rate that will be used by all financial institutions for any retail floating-rate loans applied after 1 August 2022. Typically, this would affect mortgage loans and personal loans.

A floating-rate loan is also known as a variable rate, whereby the interest rate will rise or fall depending on specific financial benchmarks.

For loans applied and approved before said date, these existing loans would still follow the BR/BLR until repaid in full.�However, just like the SBR, it will move together with the OPR after 1 August.

Why Was SBR Introduced & How Does It Benefit Me?

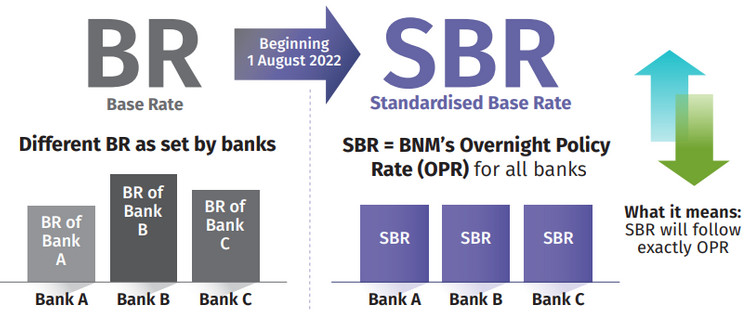

During the times of Base Rate, financial institutions would use different methods to set their base rate. Thus, you’d see situations where bank A offers 2.57%, bank B offers 2.63%, and bank C offers 1.75%. The various rates can be puzzling for customers to compare and calculate their loans accurately, which is where the SBR comes in.

Now, with the SBR attached solely to the OPR, any changes to your loan’s interest rate would only happen if the OPR takes a hike or gets cut. Other contributing factors are if your credit risk has increased because of late repayments, higher bank operating costs, etc. that would affect the spread added to the SBR.

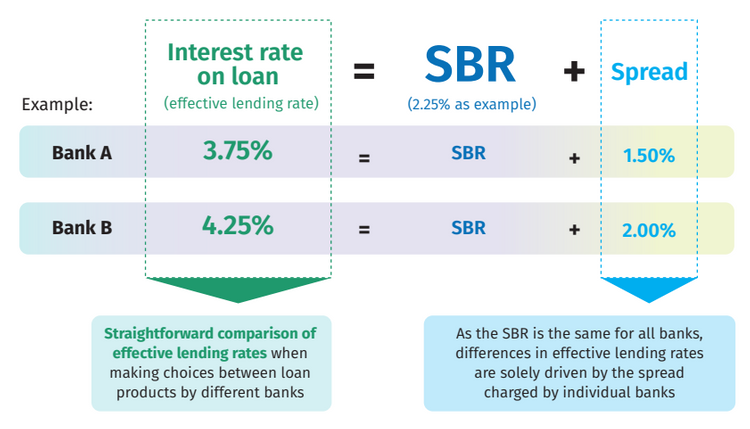

Here’s a rough idea of how banks will use the SBR to quote their lending rates:

Reference Rate (eg: SBR of 2.25%) + Spread (1.50%) = Lending Rate (3.75%)

What is this ‘spread’? Well, it’s not the type you put on your bread!

Generally fixed throughout the loan’s lifetime, a spread encompasses credit and liquidity risk premiums, profit margins, and operating costs. As we mentioned earlier, increased credit risk could also affect the spread, which affects the lending rate.

Each bank also has its own way of calculating a spread, resulting in different lending rates. However, as the SBR remains the same across the board, comparing lending rates is more straightforward now.

For consumers, the SBR allows us to make better decisions regarding loans. Undoubtedly, it also reduces the hassle of calling up banks, enquiring about their rates, and making lots of calculations to find the best interest rate and bank to choose. With the SBR, every bank will use the same single rate.

What Is The Difference Between Standardised Base Rate & Base Rate?

Implemented in 2015, the BR was an interest rate for banks to refer to before deciding on the interest rate for your mortgage. This meant they could implement their own reference rate – which is why you would see banks offering competitive ones.

Although they had the deciding power, banks were required to set these rates based on a formula by the central bank and with the BNM rate as a benchmark, so these figures aren’t being pulled randomly out of thin air.

With the SBR, banks no longer have to set the rates themselves. Instead, they will mirror the OPR and will be uniform for all banks.

How Does The OPR Hike Affect SBR?

The OPR and SBR have a linear relationship – when one rises, so will the other. In that sense, when the OPR is revised, the banks will also make adjustments to the SBR with the same amount of change in the OPR.

Even though every bank will now follow the same SBR, that doesn’t mean you should go with the first bank you see or hear. Lending rates can differ as a spread plays a part, and it’s up to the bank on how they want to calculate that, so some good ol’ research will still come in handy!

The interest rates of a mortgage loan can seem like a big chunk of your finances, but don’t forget that there are other areas where you’ll need to fork out money too. In the beginning, it’s the house downpayment and legal documents, and once your house is complete, make it a home by renovating and incorporating tasteful interior designs.