Paying Off Your Home Loan Early: Yay Or Nay?

If you have the financial capability to do so, you can actually save on tens of thousands of Ringgit! Read on to find out how different loan tenures affect the total amount you need to pay at the end of the term.

Before you can even start to feel the excitement of buying a house, you have to go through the tiring process of reviewing, researching, and choosing the best housing loan which suits your requirements.

But even that isn’t as straightforward as just walking into a bank and filling in some paperwork!

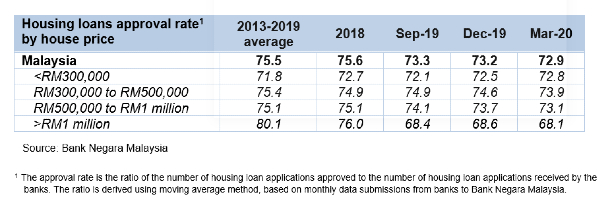

According to Bank Negara Malaysia (BNM), household loan approvals for Q2 2020 has dropped by 56.8%, with a value of RM24.8 billion, compared to RM57.4 billion in Q2 2019.

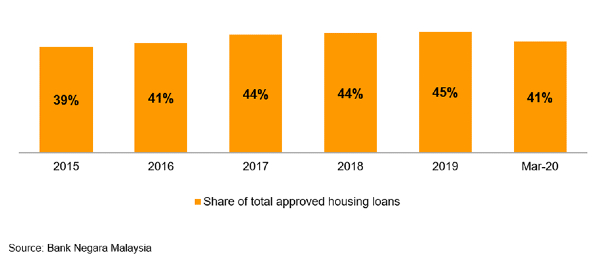

BNM says that the total applications for housing loans between January and March 2020 was at RM44.8 billion, during which the banks approved RM32 billion of home financing to about 75,000 borrowers.�From this, 41% consisted of first-time homebuyers:

The moderation in approval rate is said to be reflecting the continued housing unaffordability issue, arising from the mismatch between supply and demand of properties.

High debt, existing financial obligations, poor credit history, and insufficient documentation are just some of the more common reasons for rejection of housing loan applications.

What If I Have A Home Loan, But Want To Pay It Off Early?

Although you may have been successfully approved for a home loan (congratulations!), there’s still more for you to carefully consider.

But what else do I need to worry about? Well, you have to plan your finances on a daily, monthly and yearly basis in order to keep up with your repayments!

Once you’ve made the decision to take the obligation of a home loan, you have to bear the financial burden for quite a long time, depending on your loan tenure.

The total cost of a home loan is not just the actual value of the home, it also includes the interest you pay on the loan itself.

For example, if you take out a 30-year fixed loan, you’ll have to send a repayment amount (which covers BOTH your principal and interest) to your borrower for that amount of time – unless you decide to pay it off earlier.

One of the common questions that property owners have, is whether they should pay off their loan earlier when they have the financial resources to do so.

Ending the home loan early (if you can afford it), could be an advantage for you, especially when you are nearing retirement. Here are just some of the more common reasons for choosing to do so:

- Paying off your home loan early can give you peace of mind, and could free up some cash for travelling, retirement, or other long-term plans.

- Being debt-free, presuming that there are no other loans served, may protect you from losing your home if you run into financial difficulties.

- Depending on the type of tenure, the interest that will be potentially paid for a full-term loan might be about 30% to 50% of the house price that you purchased.

To put it simply: If you have the financial capability to do so, in the long run, you could actually be saving a whole lot of money!

According to Dr Ernest Cheong of PTL Chartered Surveyors, the obvious advantage to pay off your housing loan early is that a borrower can save on the payment of interest.

“Basically, when borrowers pay off their 30-year housing loan, they would have paid a total amount that’s triple the purchase price, on the basis of a 90% housing loan and that the instalment has been paid on time every month,” he said.

Cheong went on to elaborate that instead of paying triple the original purchase price, owners may only have to pay double if they choose to pay off within 15 years, instead of 30 years.

Let’s take a look at some sample scenarios containing different loan tenures and monthly repayment amounts, that can help us better understand the benefits and drawbacks of choosing to pay off your home loan early:

Scenario 1: 35 years

Purchase price |

RM1,000,000 |

| Housing loan (90%) | RM900,000 |

| Loan duration (years) | 35 |

| Interest per annum (%) | 4.5 |

| Monthly repayment | RM4,259 |

| Total paid at the end | RM1,788,910 |

| Total interest payment | RM888,910 |

Scenario 2: 30 years

Purchase price |

RM1,000,000 |

| Housing loan (90%) | RM900,000 |

| Loan duration (years) | 30 |

| Interest per annum (%) | 4.5 |

| Monthly repayment | RM4,560 |

| Total paid at the end | RM1,641,660 |

| Total interest payment | RM741,660 |

Scenario 3: 25 years

Purchase price |

RM1,000,000

|

| Housing loan (90%) | RM900,000 |

| Loan duration (years) | 25 |

| Interest per annum (%) | 4.5 |

| Monthly repayment | RM5,002 |

| Total paid at the end | RM1,500,748 |

| Total interest payment | RM600,748 |

Scenario 4: 20 years

Purchase price |

RM1,000,000 |

| Housing loan (90%) | RM900,000 |

| Loan duration (years) | 20 |

| Interest per annum (%) | 4.5 |

| Monthly repayment | RM5,694 |

| Total paid at the end | RM1,366,523 |

| Total interest payment | RM466,523 |

Scenario 5: 15 years

Purchase price |

RM1,000,000 |

| Housing loan (90%) | RM900,000 |

| Loan duration (years) | 15 |

| Interest per annum (%) | 4.5 |

| Monthly repayment | RM6,885 |

| Total paid at the end | RM1,239,289 |

| Total interest payment | RM339,289 |

Scenario 6: 10 years

Purchase price |

RM1,000,000 |

| Housing loan (90%) | RM900,000 |

| Loan duration (years) | 10 |

| Interest per annum (%) | 4.5 |

| Monthly repayment | RM9,327 |

| Total paid at the end | RM1,119,295 |

| Total interest payment | RM219,295 |

What Do The Experts Say About Paying Off Your Home Loan Early?

According to Cheong, when the loan repayment period is shortened by half (from 30 years to 15), the borrower, at the end of the loan period of 15 years, pays between 62% to 70% of the total amount s/he has to pay for the 30 years tenure.

“It’s definitely an advantage to pay off your home loan early, if you have the available cash to comfortably do so (just look at the increasing monthly repayment amounts in the tables above)!

“Furthermore, in these uncertain times, the earlier the borrower is free from his/her housing loan obligation to the bank, the safer s/he would be when hard times come.

“For example, when there’s a job loss or their own business takes a big hit during a global pandemic (like the one we’re currently facing), finding out that s/he is not able to afford the repayment for the home loan and therefore facing the possibility of bankruptcy is a terrifying thing,” he added.

Ron Lim Tau Loong, Mortgage Sales Department Team Manager, Hong Leong Bank, has suggested another alternative: Instead of paying off the existing home loan, borrowers can also opt to use the money to reduce or omit their interest payment (based on the daily rest interest).

Tip

The term ‘daily rest interest’ refers to a type of calculation, where your loan’s interest will be calculated based on the previous day’s outstanding balance amount.

Lim says most of the banks in Malaysia offer home loans with the daily rest interest, and borrowers can use it to their benefit.

“If the home owner decides to use his/her extra money in this manner, they can actually benefit from the daily rest interest calculation.

“This is where they deposit any available sum of cash into their home loan account, and the interest will be reduced/omitted, thereby allowing them to save a bit more on the monthly repayments,” he said.

Lim also stated that if they needed to use the money, they can withdraw at any time, and continue with the regular type of repayments – with the interest rate included to the instalment.

“Paying off totally may not be a good idea, especially in this uncertain economy. Even those who can afford to pay off, may choose to serve their monthly loan as it is, and decide to use the extra money they have for other investments which could get them better returns for their money,” he said.

He suggested that the additional cash that borrowers possess could be spent for other purposes or investments. However, he said, some might just want to be free of the burden and be debt-free, and that’s totally up to them.

“If you settle the loan with whatever extra money you have, especially if it’s a big amount, you might be in trouble when you actually NEED the cash! You can’t be selling your assets for that, right?” he questioned.

Let’s say the property price is RM1 million, and your loan amount is RM900,000. If you have RM900,000 of cash on hand, you can deposit it into your home loan account and the monthly payment deduction will be calculated according to the balance in the account.

“So, you’ll be saving on the interest payment every month and the cash in the account will be available for you anytime you need to use it,” he said.

Paying off the home loan is a dream for many homeowners. If this goal is within reach for you and your family, it might be a smart move to pay off your loan balance soonest possible.

Not only will it free up extra money every month, but it provides added financial security during a housing crisis, allows you to save more, and may even give you the chance to fulfil other dreams that need extra financial backing.

However, at the end of the day, your financial health and life circumstances will be the main factors that will determine whether paying off your home loan early is beneficial or detrimental for you.